>

The Big Definitions in Economics

When studying any subject, a key first step is to learn the lingo. Here are definitions for three of the most important words in economics:

Economics studies how people allocate resources among alternative uses. The reason people have to make choices is scarcity, the fact that we don’t have enough resources to satisfy all our wants.

Microeconomics studies the maximizing behaviour of individual people and individual firms. Economists assume that people work toward maximizing their utility, or happiness, while firms act to maximize profits.

Macroeconomics studies national economies, concentrating on economic growth and how to prevent and ameliorate recessions.

>

>

>

Macroeconomics and Government Policy

Economists use gross domestic product (GDP) to keep track of how an economy is doing. GDP measures the value of all final goods and services produced in an economy in a given period of time, usually a quarter or a year.

A recession occurs when GDP is decreasing. An expansion occurs when GDP is increasing.

The unemployment rate measures what fraction of the labour force cannot find jobs. The unemployment rate rises during recessions and falls during expansions.

Anti-recessionary economic policies come in two flavours:

Monetary policy uses an increase in the money supply to lower interest rates. Lower interest rates make loans for cars, homes, and investment goods cheaper, which means consumption spending by households and investment spending by businesses increase.

Fiscal policy refers to using either an increase in government purchases of goods and services or a decrease in taxes to stimulate the economy. The government purchases increase economic activity directly, while the tax reductions are designed to increase household spending by leaving households more after-tax monies to spend.

>

>

>

Types of Industries by Economic Definition

To help them to make sense of industries in which firms are interacting, economists group industries into three basic structures. These three structures are as follows:

Perfect competition happens in an industry when numerous small firms compete against each other. Firms in a competitive industry produce the socially optimal output level at the minimum possible cost per unit.

A monopoly is a firm that has no competitors in its industry. It reduces output to drive up prices and increase profits. By doing so, it produces less than the socially optimal output level and produces at higher costs than competitive firms.

An oligopoly is an industry with only a few firms. If they collude, they reduce output and drive up profits the way a monopoly does. However, because of strong incentives to cheat on collusive agreements, oligopoly firms often end up competing against each other.

>

>

>

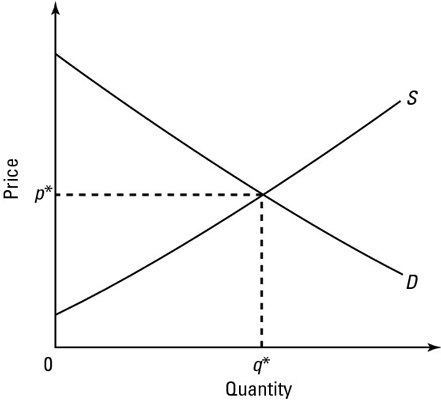

What Is Market Equilibrium?

Buyers and sellers interact in markets. The market equilibrium price, p*, and equilibrium quantity, q*, are determined by where the demand curve of the buyers, D, crosses the supply curve of the sellers, S.

In the absence of externalities (costs or benefits that fall on persons not directly involved in an activity), the market equilibrium quantity, q*, is also the socially optimal output level. For each unit from 0 up to q*, the demand curve is above the supply curve, meaning that people are willing to pay more to buy those units than they cost to produce. There are gains from producing and then consuming those units.

>

>

>

Market Failures from an Economic Perspective

Several prerequisites must be fulfilled before perfect competition and free markets can work properly and generate the socially optimal output level. Several common problems include the following:

Externalities caused by incomplete or nonexistent property rights: Without full and complete property rights, markets are unable to take all the costs of production into account.

Asymmetric information: If a buyer or seller has private information that gives her an edge when negotiating a deal, the opposite party may be too suspicious for them to reach a mutually agreeable price. The market may collapse, with no trades being made.

Public goods: Some goods have to be provided by the government or philanthropists. Private firms can’t make money producing them because there’s no way to exclude non-payers from receiving the good.

>

>

dummies

Source:http://www.dummies.com/how-to/content/economics-for-dummies-cheat-sheet-uk-edition.html

No comments:

Post a Comment